What a time it’s been for Frontdoor. In the past six months alone, the company’s stock price has increased by a massive 62.6%, reaching $55.15 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Frontdoor, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.We’re happy investors have made money, but we're swiping left on Frontdoor for now. Here are three reasons why there are better opportunities than FTDR and a stock we'd rather own.

Why Is Frontdoor Not Exciting?

Established in 2018 as a spin-off from ServiceMaster Global Holdings, Frontdoor (NASDAQ:FTDR) is a provider of home warranty and service plans.

1. Long-Term Revenue Growth Disappoints

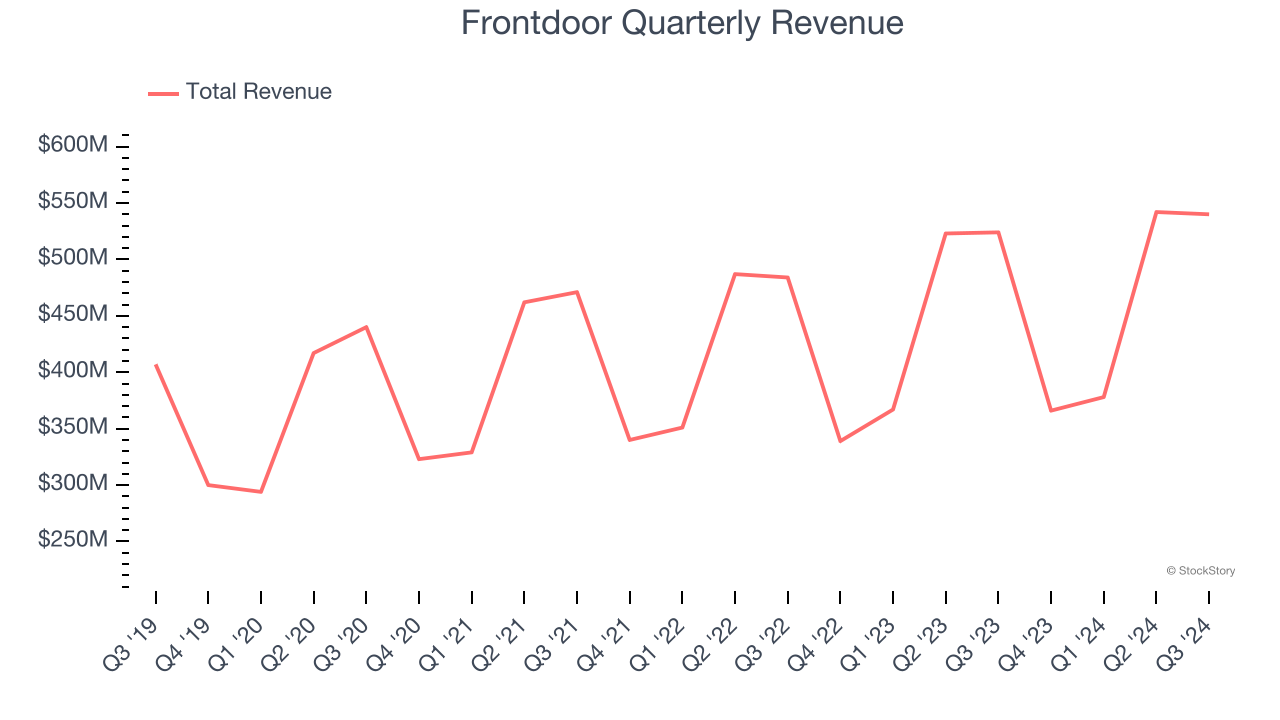

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Frontdoor’s sales grew at a sluggish 6.3% compounded annual growth rate over the last five years. This fell short of our benchmark for the consumer discretionary sector.

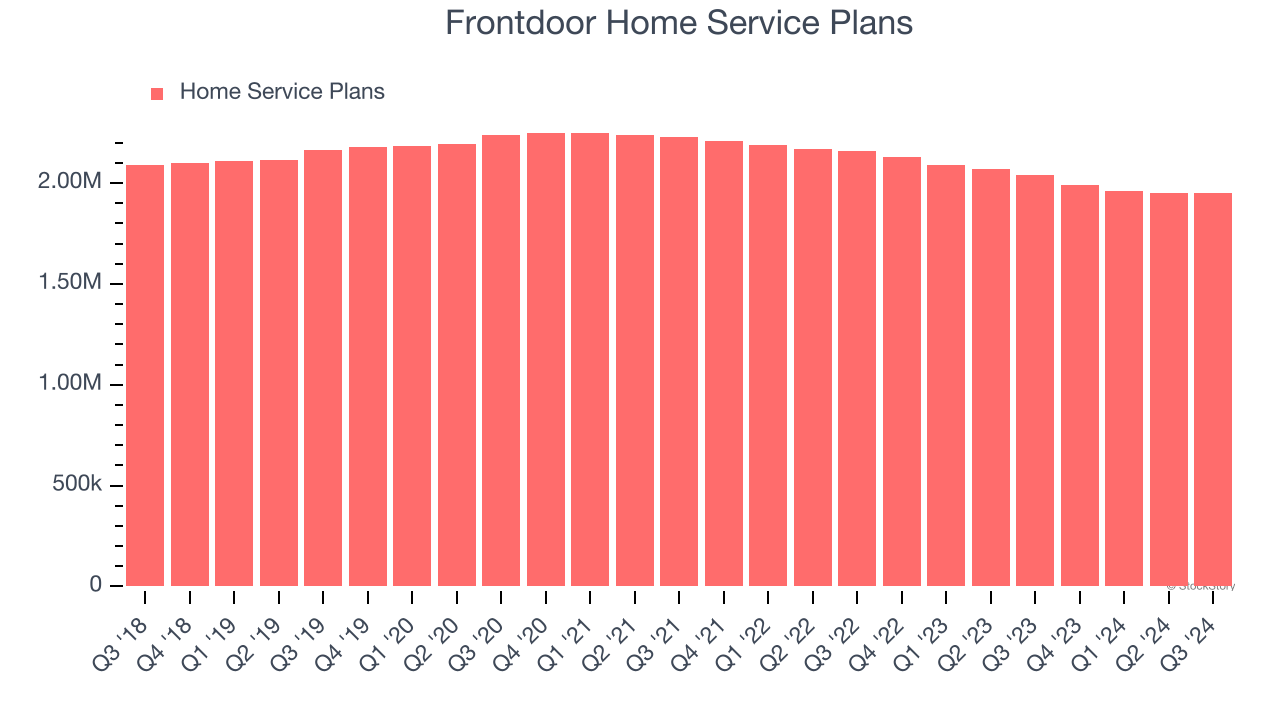

2. Decline in Home Service Plans Points to Weak Demand

Revenue growth can be broken down into changes in price and volume (for companies like Frontdoor, our preferred volume metric is home service plans). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Frontdoor’s home service plans came in at 1.95 million in the latest quarter, and over the last two years, averaged 5.2% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Frontdoor might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

3. Cash Flow Margin Set to Decline

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict Frontdoor’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 12.8% for the last 12 months will decrease to 10.7%.

Final Judgment

Frontdoor isn’t a terrible business, but it isn’t one of our picks. After the recent surge, the stock trades at 20.1× forward price-to-earnings (or $55.15 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're pretty confident there are superior stocks to buy right now. Let us point you toward Uber, whose profitability just reached an inflection point.

Stocks We Like More Than Frontdoor

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.